The licence is signed. Procurement signs off. The customer’s logo goes on the partner page. The platform books the ACV, the rep takes the commission, customer success inherits the relationship, and the economic engine for that customer is effectively complete.

What follows is retention, expansion, and renewal at roughly the same number until somebody upsells a tier.

That has been the default shape of enterprise software for two decades.

It has worked so well that almost nobody inside a software company thinks of it as a model at all. It is simply how software is sold. It is also no longer how value is created in the part of the market the legal AI platforms are operating in.

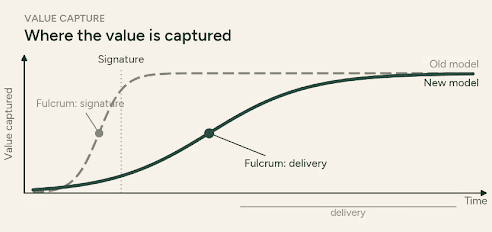

The fulcrum has moved

What has changed is where the fulcrum of value sits. For twenty years the fulcrum sat at signature. The vendor invested heavily before the contract, captured the ACV, and ran afterwards on a retention footing. Every structure inside the company, the sales org, the comp plans, the renewal motions, the success teams, the roadmap priorities, was built around that point.

In a market priced on usage, outcomes, or any of the agentic models now common in legal AI, the fulcrum moves downstream, sometimes by months, sometimes by years. Pre-signature still matters. But the bulk of the value a vendor will ever capture from a customer is now created in delivery, after the customer starts using the product.The retention question is no longer whether the customer’s workflow bent to accommodate the software. It is whether the customer got what they paid for, often enough, at the unit cost they expected.

The activation gap

Inside the platforms, the symptom of all this has a precise shape. We call it the activation gap.

The platform is sold. The seats are paid for. The pilot succeeds. Then, six to twelve months later, the customer is using 20 per cent of what they bought, the playbooks are half-configured, and the rollout has stalled at the team that ran the pilot. The renewal conversation gets harder. Net revenue retention suffers. Nobody is quite sure what broke, because the platform technically works.

What broke is not the product. What broke is the operating model around the product.

Why the operating model can’t follow

Consider how a legal AI platform is usually built inside. Sales is structured around new logos and renewals, with comp calibrated to ACV at signature. Customer success runs as a retention function, thin on headcount and light on any mandate to actually deliver work. Implementation, where it exists inside the vendor at all, is a separate motion sold separately, often months after go-live and paid for from a different budget. Product is built to be configurable rather than to be operated. The whole company is engineered around the moment of signature, because that is where the value used to sit.

This is the two-contract model that has shaped enterprise software for twenty years: one contract to buy the platform, a separate one to implement it, sometimes signed months apart, paid from different budgets, sold by different organisations. The vendor is paid to land seats. The partner, where there is one, is usually paid to bill hours. Neither is paid for the customer’s outcome, so the deployment stalls anyway, because nobody in the chain was paid to make sure it did not.

When the fulcrum moves twelve to twenty-four months downstream of signature, that design is structurally unable to capture the value that is now there. The vendor sells the seats and the customer is left to deploy. The platform is good. The customer team is willing. The work still does not get done, because nobody inside the vendor has the mandate, the unit economics, or the operational shape to make the customer use what they bought at scale.

Marketing will not fix this. The products work as advertised. What has moved out of alignment is the commercial architecture itself.

The categories next door

You can see the same force in the categories next door. Crosby, an autopilot-native firm that prices contract review for the outcome rather than the seat, announced a $60 million Series B in spring 2026.1 It has closed the activation gap by collapsing the platform and the delivery into a single contract: no implementation phase, just throughput. That route is structurally closed to the platforms already in market. To sell outcomes the way Crosby does is to compete with the law firms and in-house teams the platform sells to. The maths does not work and the channel walks.The route that does work is to keep the platform where it is and add an outcomes layer beneath it, operated by a partner. The vendor stays the customer-facing entity. The customer pays for results. The vendor reaches the work budget that sits alongside the software budget, which is the larger of the two by some distance.2 It reaches it by operating the platform the customer has already bought, rather than by selling commoditised outcomes into the market against the firms it sells to.

Telon is a services firm in its own right, and it points the partnered offering by design rather than by limitation, to expand what the customer does with the platform it already owns. The activation gap closes. The channel stays intact, because nobody is selling NDAs-as-a-service in the vendor’s name. The data flywheel keeps running through the platform.

This is the new fulcrum the platforms have to operate, and most of them are not built to operate it alone. The systems integrators and Big Four firms are scaling fast on the largest AI engagements, but their deal sizes and unit economics are built for a different shape of work.3 The autopilot-native firms compete with the platforms’ own customers. The aggressive consolidation route, which Eudia has shown can be made to work with a $105 million Series A, is not a move most platform CEOs can take to their boards.4 I will take each of these apart in the essays that follow.

The shape that’s missing

What the market needs, and what does not yet exist in the right shape, is a new kind of services firm, AI-native and built to operate the new fulcrum rather than retrofitted to it: agentic delivery from day one rather than retrofitted from a billable model; teams that pair deep legal expertise with applied AI fluency; a commercial structure that aligns the vendor’s economics with the partner’s instead of competing for the same budget; and an IP framework that protects the platform’s flywheel while letting the partner build capability across vendors.

That is the company we are building. Telon is an AI-native legal services firm, built to sell legal work the way the market now buys it: by the outcome, delivered agentically. We start at the activation layer the platforms cannot operate alone, because that is where the value has moved.

The logic is not new, only its application to legal. The case that the next generation of large services businesses will be built AI-native, selling outcomes rather than hours and reaching the market through the software vendors they sit beside, is now well made.5 Telon is that case applied to legal and contracting: an AI-native services firm in the lineage of the ALSPs, built agentic-first, channel-aligned rather than channel-competing.

I have spent almost fifteen years in legal services delivery from three vantage points that, between them, show the activation gap from every side. As US Managing Director of LOD I built the offshore and nearshore models that helped define the ALSP category. As COO and Chief Legal Engineer at SYKE I worked directly with legal AI platforms and their customers on the gap between what was sold and what got deployed. As a Partner at PwC until earlier this year I saw how the Big Four think about scaling legal AI implementation, and learned a great deal from colleagues whose work I will go on recommending for a long time.

The observation that prompted the company is simple. The fulcrum has moved. The value of an enterprise software sale is no longer locked at signature, and the market is now paying for delivery. Most platform operating models have not caught up, because they were calibrated to the old fulcrum. The delivery problem is going unowned. That is the gap Telon is built to close.

If you are a platform CEO whose board is asking what you intend to do about the foundation model providers, the autopilot-natives, or your renewal cohort, this is one answer worth a conversation. If you are a GC eighteen months into a deployment that has not moved your backlog, it is worth a conversation too.

The market has moved. Most platforms have not. Telon is built for the gap in between.

Lewis Bretts is the CEO and co-founder of Telon. Previously US Managing Director at LOD, Partner at PwC, and COO / Chief Legal Engineer at SYKE.

1 Crosby Legal, “Series B and Planting our Flag,” Crosby blog, March 2026; additional coverage, Law.com, 31 March 2026.

2 Sequoia Capital, “Services: The New Software,” March 2026, for the relative scale of the work budget versus the software budget.

3 Benedict Evans, Spring 2026 AI presentation (ben-evans.com/presentations), for the Accenture generative AI figures.

4 Eudia $105m Series A led by General Catalyst, February 2025; Bloomberg and PR Newswire coverage.

5 Jake Saper and Jake Cohen, Emergence Capital, “The Death of Deloitte: AI-Enabled Services Are Opening a Whole New Market,” April 2024; and “Services: The New Software,” Sequoia Capital, March 2026.